Best high yield checking account: 8% Yield

In this post, I’m going talk about the best high yield checking account you can sign up for. Learn the pros/cons of using this checking account, and the risks you should consider.

Edit: This method no longer works for US-based folks. This is because BlockFi has said as of February 2022, the US no longer allows them to do business here.

Hopefully, they can cut this red tape eventually and we can all not go broke by inflation.

Table Of Contents

The Best High-Yield Checking Account

I’ll be only talking about one option here, because I don’t really believe in “top 25” lists. Such lists are overwhelming, and by definition, there’s no “25 best” of anything – if there are 25 competitors for the same thing, they’re all mediocre at best.

So let me just introduce the best high-yield checking account to you so you don’t have to wade through a bunch of low-yield, useless information.

And while what I’m about to introduce isn’t technically a “checking account” – it’s close enough in that you can liquidate and spend the money any time you’d like. There’s no:

- Restrictions on the number of times you can withdraw each month.

- Restrictions on minimum balance.

Get Up To 8% APR

So what is this magical, best “high-yield checking account” I’m talking about? I’m talking about BlockFi.

BlockFi is a cryptocurrency staking platform – and before you jump out of this page, yelling “cryptocurrency isn’t real!” – hear me out. Because you can stake crypto in coins that are pegged to the USD and isn’t volatile.

But first, what is staking? Staking is just the process of lending your money in a pool so that there’s liquidity for people to trade. So for example:

- There’s a pool of $10 million USDC that people can trade with on BlockFi.

- And another pool of ETH that’s worth $5 million.

- Say a user wants to trade a million worth of ETH for a million worth of USDC.

- The pool of ETH would now be worth $6 million. And the pool of USDC will be worth $9 million. This is because he’ll put $1 million worth of ETH in the ETH “pool” and take out $1 million worth of USDC in the USDC “pool”.

- Notice that if the USDC “pool” of money in BlockFi was less than $1 million, this trade couldn’t be easily done.

When you stake USDC, for example, you’re merely adding your money to that pool so people can trade. To incentivize you for staking, you get rewarded an APR percentage where you’ll compound the coin you staked.

Where does the high-interest APR come from? Is this a ponzi scheme? No. The high-interest APR varies. And BlockFi has a chart of the different yields here. Yields are determined by:

- Transaction fees.

- Volume of trades.

As a contrived example:

- Say the USDC trade volume in a year is $1 billion.

- And say the transaction fees for the traders is 1%.

- BlockFi will have $10 million to split between itself, and the people who staked in the pool.

- Even though the trade volume is $1 billion, your pool could be as small as, say, $100 million only.

- Thus, the $10 million cash flow represents a 10% return in a year. BlockFi might keep 2% of that money and then the other 8% is paid out to the stakers.

What Should You Stake In?

There are a few coins tied to the USD, which you could stake in. Unlike ETH or any other coins, these are almost always going to be tied to $1, or very close to $1 (like $1.02). Hence, you can enjoy the high volume of cryptocurrency trading without being exposed to its volatility.

Therefore, I wouldn’t recommend staking in highly volatile coins and would recommend you only stake in coins that are pegged to the USD. This is because you want to use this as a ‘checking’ account, and not an investment account. Therefore, your ‘portfolio’ shouldn’t be exposed to market volatility.

As of this writing, if you look at the payout rates here, you’ll find the following coins (pegged to USD) yielding the following interests:

- USDT tier 1 (20K or below), 8%.

- USDC tier 1 (20K or below), 8%.

- BUSD tier 1 (20K or below), 8%.

- DAI tier 1 (20K or below), 8%.

- PAX tier 1 (20K or below), 8%.

- GUSD tier 1 (20K or below), 8%.

If you throw 20K in each of these 6 different coins, you’d get 8% annually on a $120K principal. Or $9600 in dividends. Not bad.

But what if you have a lot more money? Each of these coins drop off to 7% up to 10 million each. So you can in theory throw in up to 60 million dollars and still yield 7% annually, or $4.2 million in annual cash flow. Caveat: if you throw that much money in, it’s likely you’ll change the market and the rates that the site offers.

Pros And Cons Of This “Best High Yield Checking Account”

Pros:

- High yield. 8% up to 120K. And 7% up to 60 million.

- These coins are pegged to the USD, so you get the upside of trading volume, without the downside of crypto volatility.

- Taking advantage of this asymmetry gives you high yield and is the best way to use this as a checking / savings account.

Cons:

- They can change the rates at any time. For example, I used to stake BTC there at 6%. Now it’s at 0.1%.

- Thus, your 8% can change over time.

- Though this isn’t different than any other checking / savings account. I used to “stake” my USD in Ally at 2% APR, but now it’s just at 0.5%. So banks don’t protect you from rate volatility either.

- Not FDIC insured, so you don’t bet the farm on it. If BlockFi goes bust or there’s a massive run, you might not be able to get any of your money back.

In Conclusion

BlockFi is a great platform to get 8% on your money (as of this writing). If you sign for BlockFi, I wouldn’t recommend staking your money in anything other than coins that are pegged to USD. Staking in non-pegged coins is extremely risky and I would consider that as just crypto-investing, as opposed to using BlockFi as a high-yield checking account.

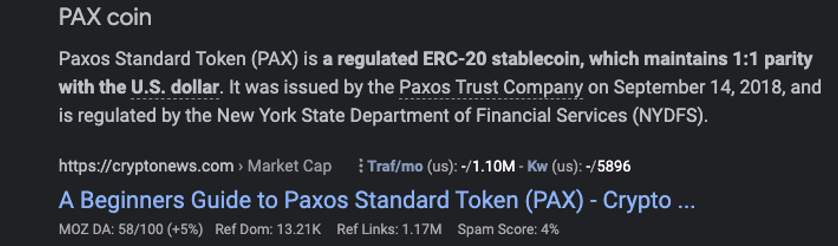

You can tell which coins are pegged to USD by simply googling it. For example, if you don’t know what “PAX coin” is, simply Google it and it’ll tell you that it’s 1:1 to USD:

As rates and legislature around these coins can change at any time, I wouldn’t put all your savings to try and chase this 8% yield. It’s safe that it’s pegged to USD, but it’s not safe because nobody can tell the future nor know how things to develop. Thus, as a good practice, you shouldn’t throw “all your money” at anything, no matter how “safe” it looks. Other words, never YOLO.

My recommendation is to diversify this best high-yield checking account with, say, uncorrelated high-yield dividend stocks. And DYOR. This isn’t investment advice, etc.

But on a positive note and how this will work practically is like this: as the coins you’ll stake in is pegged to USD and isn’t volatile, you can – at any time – just liquidate your position to USD and use it as spending money.

P.S: If you sign up with my referral link above, you’ll get up to $250 in Bitcoin when you buy crypto with BlockFi. You can just buy USDC or some other coin pegged to the USD and it should still count. The signup link for BlockFi is here in case you missed it.

0 Comments